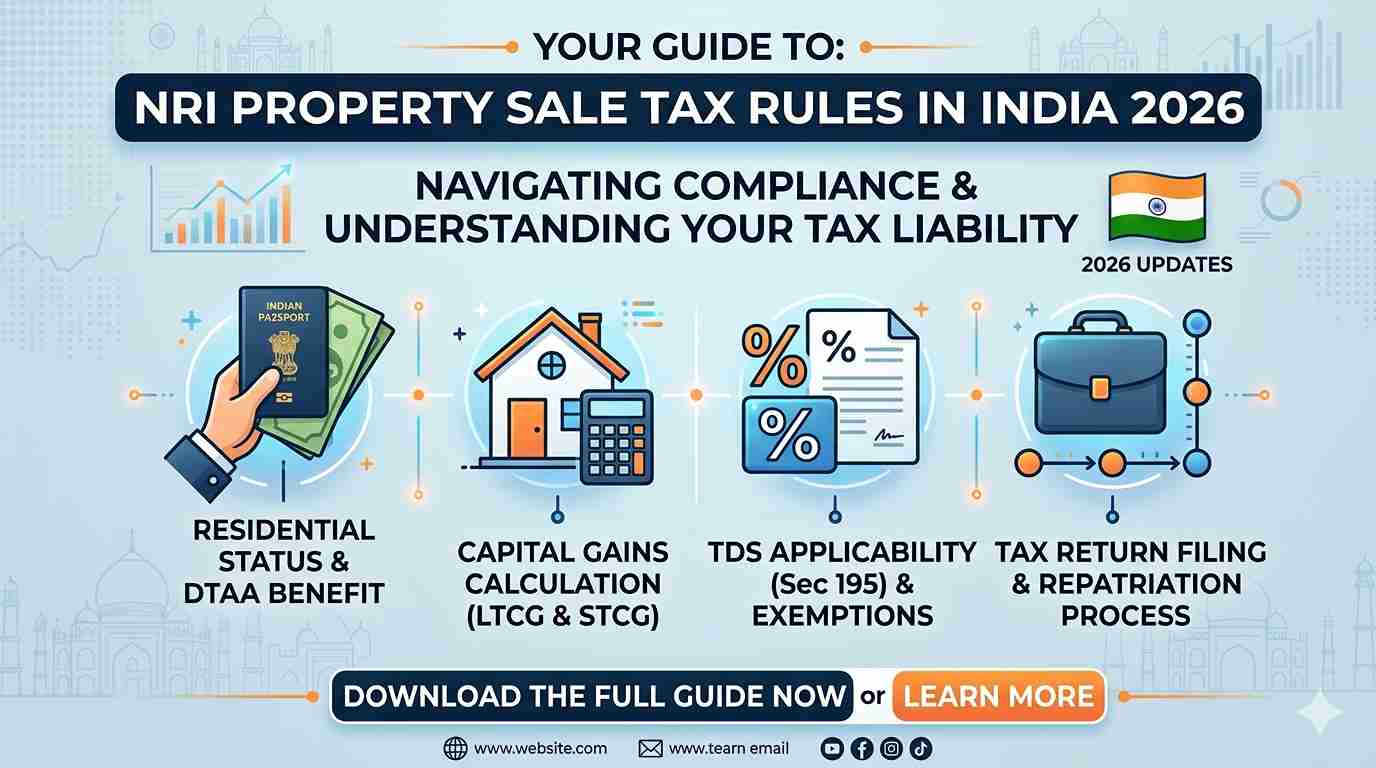

Selling property in India as an NRI can unlock significant funds, but it comes with important tax obligations and repatriation procedures under the Income Tax Act, FEMA, and RBI guidelines. In 2026, a key simplification from Budget 2026 makes the process easier for buyers and sellers alike.

Whether you own an apartment in Hyderabad, a villa in Bangalore, or a flat in Mumbai, understanding these rules helps you minimize tax outflow, avoid delays, and repatriate your hard-earned money smoothly back to the USA, UAE, UK, or elsewhere.

Budget 2026 Update: Simplified TDS Compliance for NRI Property Sales

One of the most welcome changes in Union Budget 2026-27 is the removal of the TAN (Tax Deduction and Collection Account Number) requirement for resident buyers purchasing property from NRIs.

- Effective from 1 October 2026, buyers (individuals and HUFs) can deduct and deposit TDS using their existing PAN instead of obtaining a TAN.

- This aligns NRI property sales with regular resident-to-resident transactions, reducing paperwork and delays.

- Important: TDS rates and capital gains tax rules remain unchanged. The change is purely procedural.

This reform benefits NRIs by making deals more attractive to Indian buyers and speeding up closings via Power of Attorney (PoA).

Capital Gains Tax on Property Sale for NRIs (2026 Rules)

When you sell property in India, you pay tax on the profit (capital gains). The tax treatment depends on the holding period.

| Holding Period | Type of Gain | Tax Rate (2026) | Indexation Benefit | Key Notes |

|---|---|---|---|---|

| Up to 24 months | Short-Term Capital Gain (STCG) | Taxed at your applicable slab rates + surcharge + 4% cess | No | Higher effective rate possible |

| More than 24 months | Long-Term Capital Gain (LTCG) | 12.5% (without indexation) + surcharge + 4% cess | Not available for most post-2024 acquisitions | Exemption options available |

Note: For properties acquired before the Budget 2024 changes and sold in 2026, the new 12.5% LTCG rate without indexation generally applies. Always calculate exact gains with a CA.

TDS on Sale of Property by NRI (Section 195)

The buyer must deduct TDS on the full sale consideration (not just the profit) before paying you.

- LTCG (held > 24 months): Base TDS around 12.5% + surcharge + cess (effective rate varies; often 13–15%+ depending on income).

- STCG (held ≤ 24 months): TDS at slab rates, which can reach up to 30% + surcharge + cess.

TDS is deposited by the buyer, who issues Form 16A to you. You can claim credit or refund of any excess TDS when filing your Indian Income Tax Return (ITR).

Pro Tip: Apply early for a Lower or Nil TDS Certificate under Section 197 (via Form 13) if your actual tax liability is lower (e.g., due to exemptions under Section 54). This improves cash flow and reduces refund hassles. Processing can take 2–4 weeks, so plan ahead.

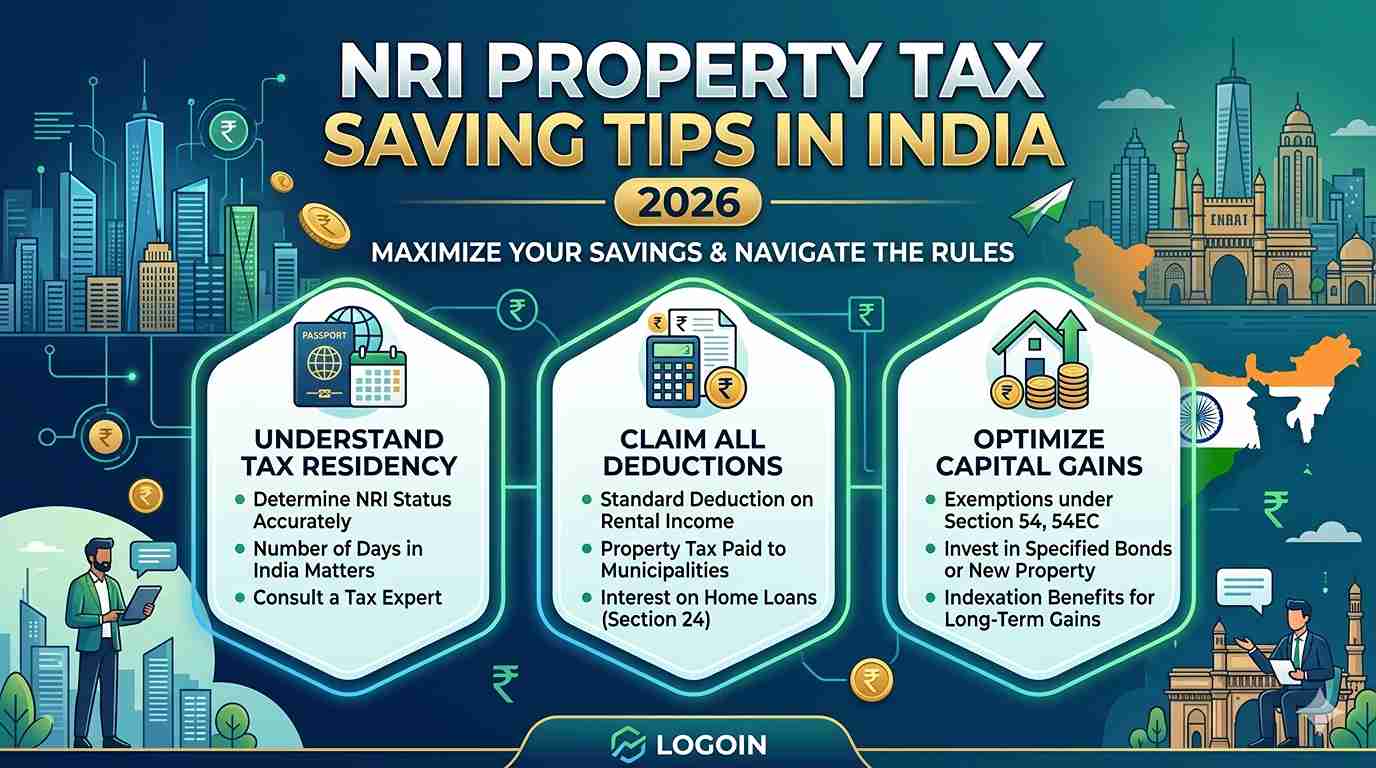

How NRIs Can Save or Exempt Capital Gains Tax

You can legally reduce or eliminate tax liability through exemptions (available for long-term gains):

- Section 54 — Reinvest the capital gains (not full proceeds) in one or two new residential properties in India.

- Buy within 2 years or construct within 3 years of sale.

- Maximum exemption limit: ₹10 crore.

- Section 54F — If selling a non-residential asset, reinvest the net sale proceeds in a residential house in India (subject to ₹10 crore cap).

- Section 54EC — Invest up to ₹50 lakh of long-term capital gains in specified bonds (NHAI, REC, etc.) within 6 months. 5-year lock-in period.

Capital Gains Savings Account: If you cannot reinvest immediately, park the gains in this account to claim exemption later.

Repatriation Rules for Property Sale Proceeds (FEMA/RBI Guidelines)

After the sale, you can repatriate (transfer abroad) the net proceeds, subject to these rules:

- Sale proceeds must first be credited to your NRO (Non-Resident Ordinary) account.

- Repatriation Limit: Up to USD 1 million per financial year (April–March) per person from the NRO account. This covers property sale proceeds, rental income, and other eligible funds.

- Lifetime Restriction: Repatriation of residential property sale proceeds is generally allowed for a maximum of two properties in a lifetime (if originally purchased with foreign funds or via NRE/FCNR).

Documents Required for Repatriation:

- Proof of tax payment / TDS deduction.

- Form 15CA (online declaration by the remitter on the Income Tax portal).

- Form 15CB (Chartered Accountant certificate confirming tax compliance, DTAA benefits if any, and FEMA adherence). Note: Some references mention updated Form 145/146 effective from April 2026 in certain contexts — confirm with your CA/bank.

- Sale deed, bank statements, and CA-certified computation of capital gains.

Banks usually process repatriation within 3–10 working days once documents are complete. Always pay applicable taxes before repatriation.

DTAA Benefits: Claim relief or credit in your country of residence (USA, UAE, UK, etc.) for taxes paid in India to avoid double taxation. File Indian ITR even if no additional tax is due to claim refunds of excess TDS.

Step-by-Step Process for NRI Property Sale in 2026

- Engage a local lawyer and CA experienced with NRI transactions.

- Obtain PAN (mandatory) and verify property documents.

- Apply for Lower TDS Certificate (if needed) under Section 197.

- Execute sale agreement and registration.

- Buyer deducts TDS (using PAN post-Oct 2026) and pays balance amount to your NRO account.

- File ITR in India, declare gains, claim exemptions/refunds.

- Prepare Form 15CA + 15CB with CA help.

- Submit to bank for repatriation (within USD 1 million limit).

Common Pitfalls to Avoid

- Delaying Lower TDS application → excess deduction and long refund waits.

- Not maintaining proper documentation for DTAA or repatriation.

- Mixing NRE/NRO funds incorrectly.

- Ignoring ITR filing → loss of refund claims.

Recommendation: Always consult a Chartered Accountant specializing in NRI taxation and a FEMA-compliant advisor before finalizing the sale. Rules can have nuances based on your residency status, country of residence, and property details.

Ready to sell your Indian property? Start by reviewing your holding period, calculating potential gains, and connecting with an NRI-friendly CA for personalized planning.

Have you sold property in India as an NRI? What challenges did you face with TDS or repatriation? Share your experiences in the comments below.

For more practical NRI resources, explore these related guides on NRIGlobe.com:

- Tax Optimization Strategies for NRIs Owning Property in India 2026

- Best Cities for NRIs to Invest in Indian Real Estate 2026

- Complete Guide to Buying Property in India as an NRI

This article provides general information based on tax and FEMA rules as of 2026. Tax laws are subject to change. It is not a substitute for professional advice. Consult a qualified Chartered Accountant and legal expert for your specific situation.