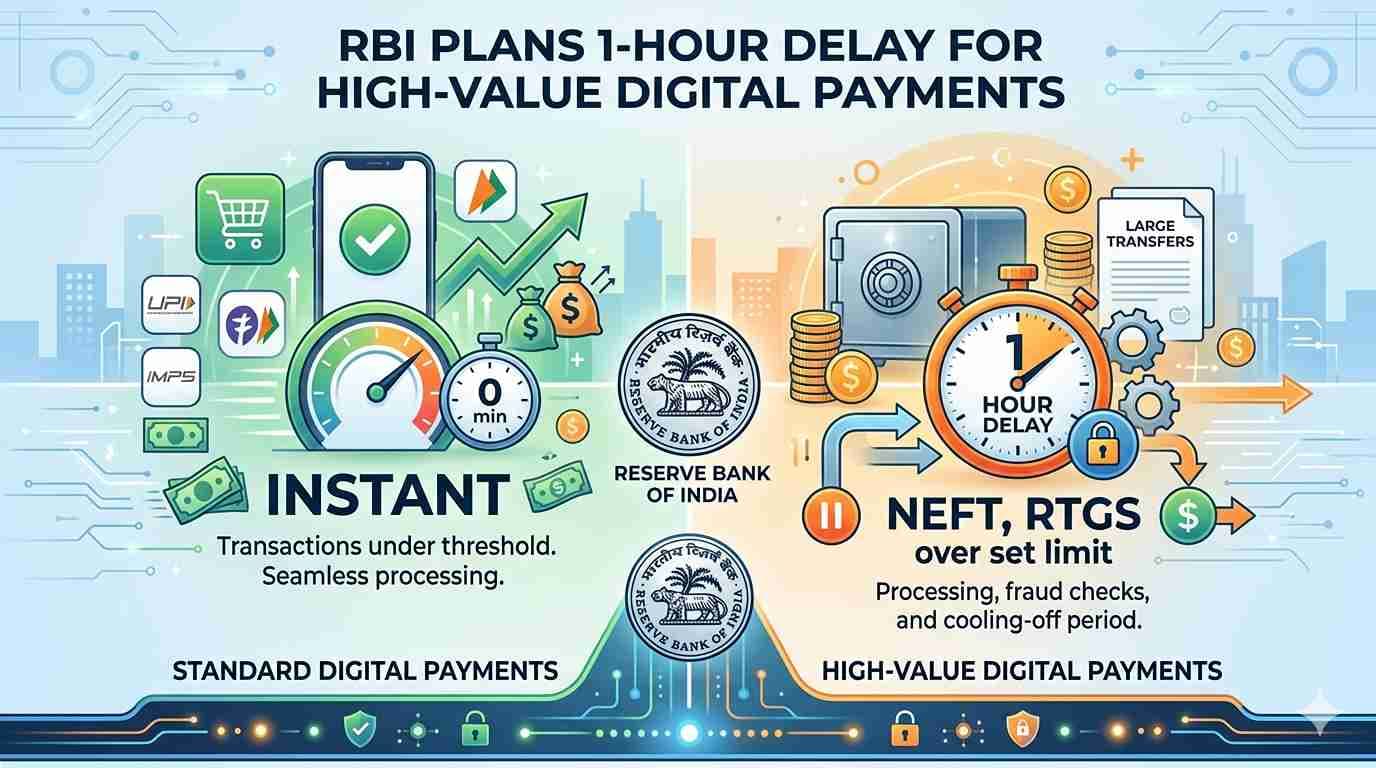

New Delhi, April 10, 2026 – The Reserve Bank of India (RBI) has released a discussion paper proposing significant new safeguards for digital payments to combat the alarming rise in fraud cases. At the centre of the proposal is a mandatory one-hour delay (cooling-off period) for high-value peer-to-peer (P2P) and account-to-account transfers exceeding ₹10,000 made via UPI, IMPS, or similar instant payment systems.

This move comes as digital payment fraud in India has skyrocketed. According to data from the National Cyber Crime Reporting Portal (NCRP), reported fraud cases surged from 2.6 lakh worth ₹551 crore in 2021 to nearly 28 lakh cases amounting to ₹22,931 crore in 2025. High-value transactions (above ₹10,000) constitute only about 45% of fraud cases by volume but account for a staggering 98.5% of the total monetary losses.

Key Proposals in the RBI Discussion Paper

The RBI has outlined four major safeguards for public consultation:

- One-Hour Delay on High-Value P2P Transfers

- All account-to-account transfers above ₹10,000 will have a 60-minute lag before the funds are credited to the recipient.

- During this window, the sender can review the transaction and cancel it if it appears suspicious.

- Important for NRIs: This delay will not apply to merchant payments (P2M), recurring payments, or whitelisted frequent payees (such as family members you regularly send money to). You can also maintain a list of trusted beneficiaries to avoid delays for routine remittances.

- Extra Protection for Senior Citizens & Vulnerable Users

- For transfers above ₹50,000, senior citizens (aged 70+) and persons with disabilities may need approval from a nominated “trusted contact” (which could be a family member abroad).

- This feature is optional and can be opted out of with proper risk acknowledgment.

- Tighter Monitoring of Suspicious Accounts

- Banks may impose limits on credits into accounts flagged for suspicious activity (commonly known as “mule accounts” used by fraudsters).

- Customer ‘Kill Switch’

- A simple one-click option for users to instantly freeze or disable all digital payment channels linked to their account in case of suspected fraud or coercion.

Special Relevance for NRIs and Overseas Indians

Many NRIs regularly send money back to India for family support, property purchases, investments, or emergencies using UPI, international remittance apps, or linked Indian bank accounts. While the proposal mainly targets domestic P2P transfers, it will indirectly affect NRIs in the following ways:

- Family remittances above ₹10,000 may face a short delay unless the recipient is added to your whitelist of frequent payees.

- NRIs with elderly parents in India will benefit from the trusted contact approval feature, adding an extra layer of safety against phone scams and impersonation frauds targeting seniors.

- The kill switch could be particularly useful for NRIs who manage Indian bank accounts remotely and want immediate control during any security breach.

- Low-value transfers and merchant payments (shopping, bills, online purchases) will continue to remain instant.

The RBI has clarified that the goal is to introduce “targeted friction” only in high-risk transactions while preserving the speed and convenience of India’s world-leading digital payment ecosystem.

Next Steps

- The RBI has invited comments and feedback from all stakeholders, including banks, fintech companies, and the public (including NRIs), until May 8, 2026.

- Feedback can be submitted through the RBI’s Connect 2 Regulate portal.

- After reviewing responses, the RBI is expected to issue final guidelines for implementation.

NRIGlobe Takeaway

While some NRIs may find the one-hour delay slightly inconvenient for urgent high-value transfers, the proposal is widely seen as a necessary step to protect families in India from sophisticated social engineering scams. With fraud losses crossing ₹22,000 crore annually, these measures could save thousands of Indian families — including those supported by overseas Indians — from devastating financial losses.

What do NRIs think? Will you support the one-hour cooling period for high-value UPI transfers? Have you or your family in India faced any digital payment fraud? Share your views and experiences in the comments below.