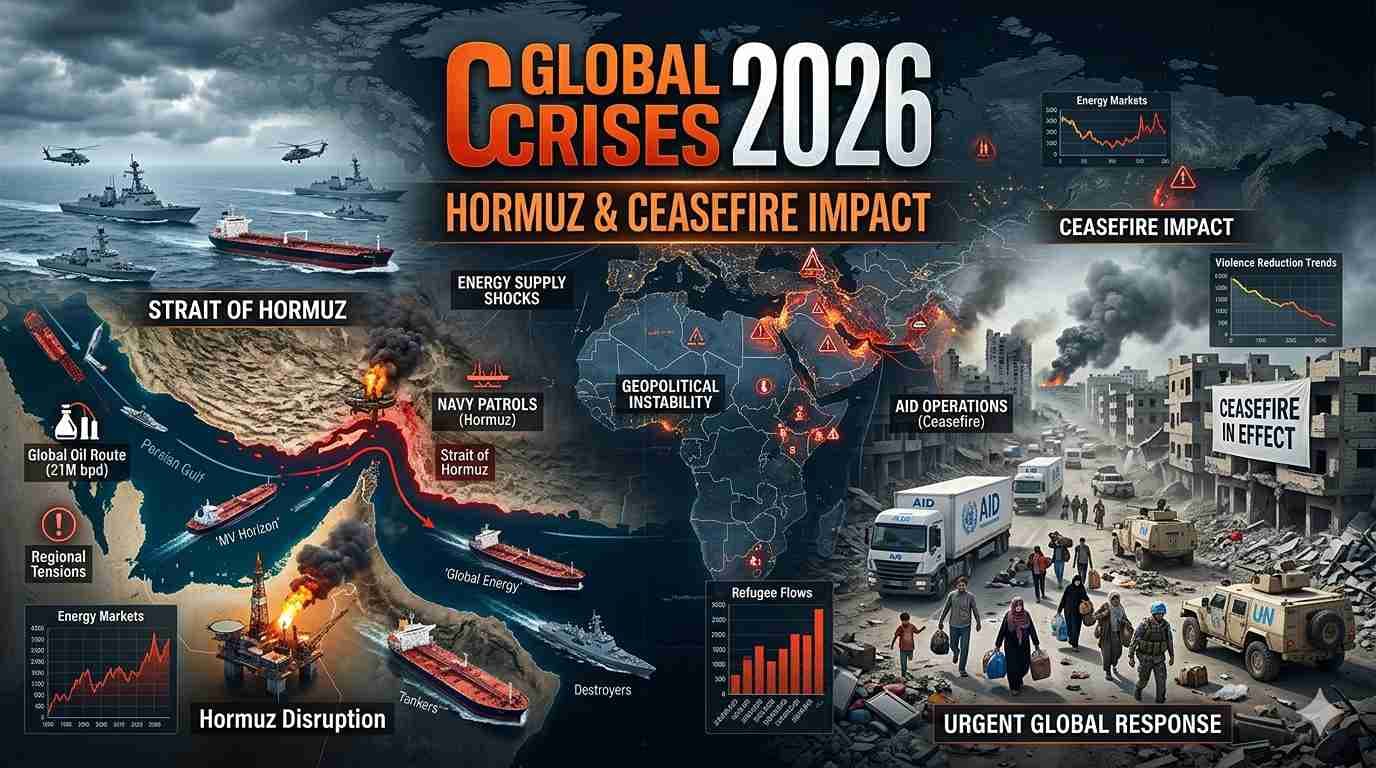

The Strait of Hormuz — the narrow waterway between Oman and Iran through which roughly one-fifth of global oil consumption physically transits — has been at the centre of the broader US-Iran-Israel tensions of 2026. For India, which imports a substantial majority of its crude oil and where the Gulf corridor remains a primary diaspora-and-trade artery, any sustained disruption in Hormuz has direct consequences for household economics — both inside India and for NRIs whose remittances and investments connect to the Indian economy. This piece walks through what the structural pathways actually are and what NRI households should monitor as the situation evolves. It builds on NRI Globe's earlier Iran War 2026 impact piece with a closer look at the Hormuz-specific channel.

Why Hormuz matters: the structural pathway

Hormuz transits approximately 20 percent of global oil consumption in normal times. India sources a meaningful share of its crude imports from Gulf producers whose exports physically pass through the strait — Iraq, Saudi Arabia, UAE, Kuwait, Qatar all rely on Hormuz transit for their seaborne exports. Any sustained disruption — even short-of-closure tensions that produce shipping insurance premium spikes — translates into higher landed crude prices in Indian ports.

The pathway from there to Indian household economics is direct: higher crude → higher refined fuel costs at the pump → higher transport costs across the supply chain → higher consumer inflation → pressure on the rupee → pressure on the current-account deficit. The household-level visibility is the petrol/diesel price at the pump and the steady rise in everyday goods costs over the following weeks.

What NRI households should monitor

Oil-price levels (Brent + WTI)

Brent crude pricing is the cleanest leading indicator. Sharp moves above prior bands signal that markets are pricing in supply-disruption risk; sustained moves indicate that the risk is becoming structural rather than transient. NRI households watching this from outside India have visibility through standard financial news sources.

Rupee-dollar exchange rate

The rupee responds to oil-import pressures with a typical lag of days to weeks. NRIs sending remittances home receive a near-real-time signal through the conversion rate they get on their next remittance. Households doing structured monthly remittances may consider front-loading or back-loading transfers based on the prevailing rupee direction — though the discipline of regular cadence usually beats timing.

Indian equity market reaction

Sectors most exposed to oil-price shocks — oil marketing companies, transport, aviation, paint and chemicals, FMCG — typically lead the index reaction. NRI investors with exposure to Indian equities through direct stocks or mutual funds may see short-term volatility concentrated in these sectors. NRI Globe's allocation framework piece on real estate vs stocks vs gold covers the broader portfolio-hygiene discipline that applies regardless of any single sector's short-term move.

Gulf-side employment indicators

For NRI families in the Gulf, the second-order signal is local employment-sector activity. Construction, oil-services, hospitality and retail in the Gulf are sensitive to regional instability. Sustained Hormuz tensions can affect project timelines, hiring cycles and salary-payment timing.

Impact on different NRI segments

- US-resident NRIs: Indirect exposure mainly through Indian-equity holdings and remittance conversion rates. Direct US-side impact through wider energy-sector inflation and any global-market risk-off response.

- UK and EU-resident NRIs: Similar indirect exposure plus more direct fuel-price impact on local life. UK households additionally tracking the broader sterling-rupee dynamics on remittances.

- Gulf-resident NRIs: The most direct exposure. Local-economy linkages, project-timeline sensitivity, evacuation-planning context. NRI Globe's earlier piece covers the practical Gulf-NRI checklist.

- Returning-to-India NRIs: Indian inflation trajectory matters more for the return calculation than for stay-abroad households. A sustained inflation push affects everything from housing costs to schooling fees to daily living expenses.

What action makes sense

The practical action items, ordered by impact-per-effort:

- Build the 6-12 month emergency cash buffer if it isn't already in place. The Hormuz situation is one of several reasons; emergency cash discipline is good regardless.

- Review the next 3-6 months of planned remittances. Currency-conversion timing matters; structured monthly cadence typically beats one-shot lumps in volatile environments.

- Review concentration risk on oil-sensitive sectors in any Indian-equity holdings. Rebalance if individual sector exposure has drifted high.

- For Gulf-resident households, confirm passport / OCI / visa documentation is current and that the MADAD portal (MEA) registration reflects current addresses.

- Stay grounded in the timeline. Hormuz situations have historically resolved in weeks to months rather than years. The base case is not closure; the base case is elevated risk premium with periodic flare-ups.

The longer-term framing

India has navigated similar Gulf-tensions in the past with mixed success — usually managing the short-term impact through strategic reserves, diversified import sourcing and diplomatic balance, while accepting the longer-term cost of currency pressure and growth-rate impact. The 2026 episode is unlikely to be different in structure, though the specifics vary.

For NRI households, the discipline that has held up well across previous episodes is the same: maintain emergency-cash buffers, avoid making large irreversible decisions in the heat of any single news cycle, and continue the regular financial-planning cadence rather than letting any one episode reset the household plan.

Sources: market data from publicly available financial reporting (Reuters, Bloomberg, FT) as of mid-June 2026; geopolitical context per ongoing international news coverage. Situation evolving; verify with current sources before acting on any specific number.